Armaguard and Australia’s cash future remains uncertain as the cash transit business grapples with staying afloat.

The monopoly owned by billionaire businessman Lindsay Fox has requested industry support at a meeting in October 2023. In the meeting initiated by Reserve Bank governor Michele Bullock, Armaguard told bank representatives, the RBA, and treasury officials that it did not have the funds to reinvest in the business sustainably.

Armguard also mentioned that it was concerned about the viability of its business model, citing it was at risk of stopping its services without any financial support. Armaguard currently supplies almost 90% of cash in all of Australia.

According to the company, low demand for cash and a seismic shift to digital payments have brought it to the brink of insolvency. The RBA confirmed this sentiment, claiming that only a selected group of people currently use cash in their everyday transactions.

Failed rescue deals and mergers

On June 2023, the Australian Competition and Consumer Commission (ACCC) approved the merger of Armaguard and Prosegur in an effort to save the company. Prosegur is another major player in the cash industry.

Although this merger received concerns of a total monopoly from many industry stakeholders, including Woolworths, the ACCC cited that Armaguard would likely exit the market and cause “significant disruption” to cash distribution without its green light.

However, this merger has done little to rescue the company’s bottom line. Armaguard claimed it projected to operate with a $190 million cash deficit over the next three years. A tumultuous funding negotiations ensued, with major banks and retailers scrambling to save the company.

Earlier this year, it was reported that a group of nine organisations (including Woolworths, Coles, Westfarmers, Australia Post, and the four major banks) had agreed to provide a $26 million funding deal to bail the struggling company – but this deal was made with a list of conditions.

Armaguard had to agree to the conditions within a tight timeframe, following which the deal would lapse. Additionally, the 40-page deal required Armaguard to disclose its financials to the negotiators. This deal was a point of concern for the cash distributor, who didn’t want its information used by banks to pursue their electronic payment agenda.

Not surprisingly, Armaguard rejected the lifeline. In a statement by its chief executive, Mick Cronin, the company mentioned that it was working with clients and all stakeholders for a solution.

“Armaguard rejects the timing ultimatum by the (Australian Banking Association) … (we are) working constructively with all (our) customers, including (our) retail customers, banks and other key stakeholders regarding both short-term and long-term financial solutions for the industry to remain sustainable,” Mr Cronin said.

“Armaguard continues to operate its full suite of services and is confident that over the coming months, it will get the business onto a long-term sustainable footing with appropriate support from the industry.”

The type of support sought by Armaguard is currently unknown.

The decline in cash in Australia

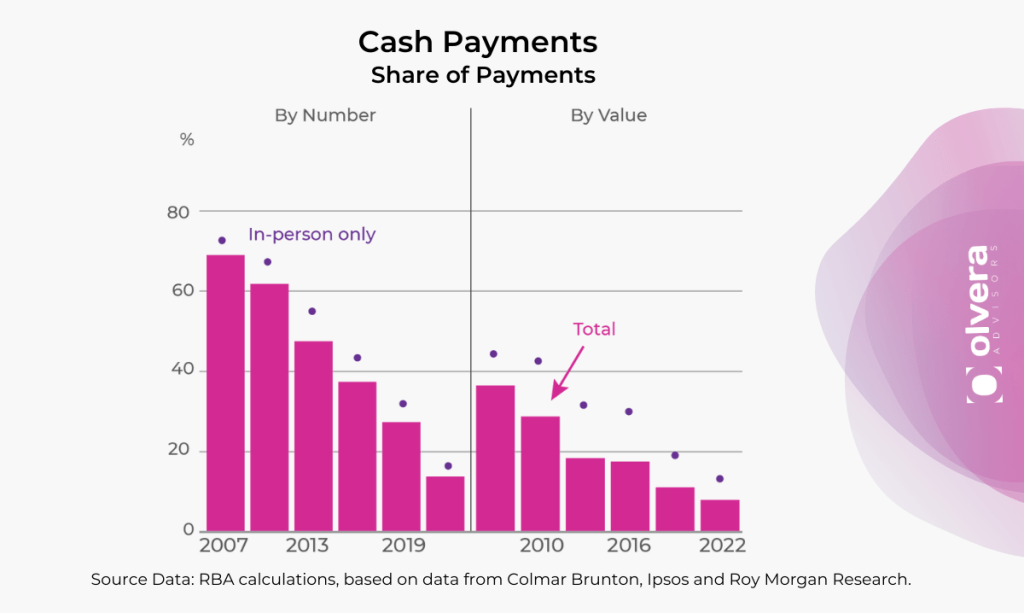

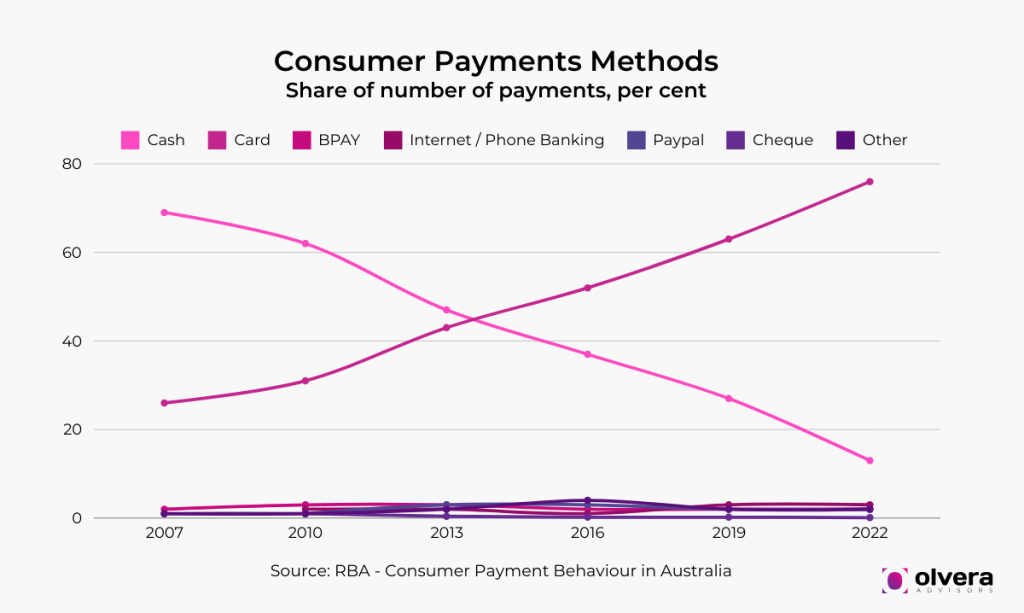

The use of cash in Australia has been in a steady and sharp decline. A study by RBA has found that in the past three years to 2022, the percentage of Australians paying with cash has halved (from 32% to 16%).

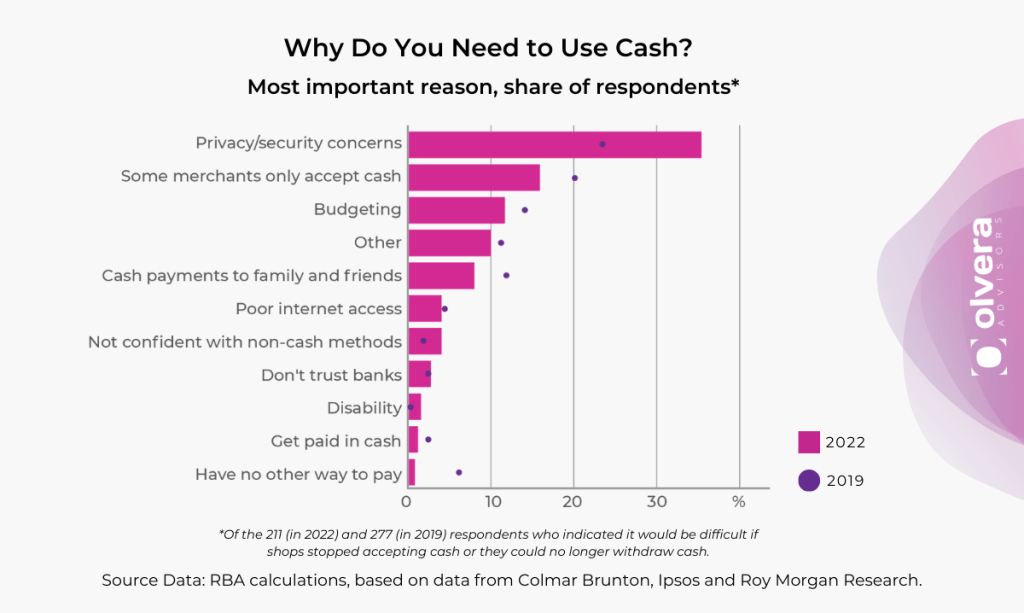

With more banks pushing for cash payments and the rise of buy-now-pay-later (BNPL) payment options, the use of the banknote has dropped significantly. However, this comes despite the value of the banknote in circulation hitting a record high last year. It suggests that consumers are keeping banknotes for emergencies, but not spending them. This corresponds to a consumer survey by the RBA, which indicates that consumers use and keep cash for security purposes.

The COVID pandemic has worsened the use of cash, as many businesses encouraged contactless payments for health purposes. In 2019, 27% of transactions in Australia were conducted in cash, but this number dropped to 18% in 2021 with the acceleration of online spending during lockdowns.

According to Mr Cronin, the decline in cash usage was still apparent even after the post-pandemic opening of retail businesses.

“The Australian cash industry has not rebounded after COVID as it has in other parts of the world. So we are in a much worse financial position than we expected when we commenced the process.”

Mr Cronin said.

Working towards a sustainable cash distribution model

Cash is still essential for businesses and consumers around the country, especially those in regional areas. According to Anna Bligh, Australian Banking Association’s chief executive, the banks will back a “sustainable model” to ensure cash continues to be available for those who need it.

“The challenge facing our economy and society is that as the use of cash for payments declines, the unit cost of transporting and distributing it escalates … ABA is seeking authorisation from the ACCC so banks can be part of the solution to design a sustainable model for people to access cash in the long-term future.” she said.

Banks and retailers are said to be working on a shared utility service to replace private cash distribution services such as Armaguard. This method is adopted by countries around the world, but its logistics might not be suitable for Australia.

“The utilities models that have worked in a couple of European jurisdictions are not challenged to get cash to somewhere like Thursday Island or Broome, or Alice Springs,” Bligh told reporters.

“That’s the challenge for a country like Australia, so I wish I could tell you I’ve found the magic bullet to that, but it’s going to take a lot of hard thinking, and we need to stabilise the cash in transit business while we do that hard thinking.”

Key takeaway

As more consumers shift towards using cash, businesses will have to choose between keeping enough cash on hand and moving towards contactless payments. Market understanding is key to ensuring that companies minimise risk and maintain efficiency.

Contactless payments have come a long way from simply tapping at a payment terminal. With the rise in digital technologies, offering consumers convenient digital payments is a way to gain more revenue. Businesses should explore options such as BNPL and loyalty apps to stay ahead of the trends and stay updated on the use of cash in Australia.

Olvera Advisors helps businesses stay ahead in a dynamic retail environment with bespoke restructuring solutions. Explore our blog for more insights on navigating the financial complexities of this dynamic industry.

Reference:

- Armaguard rescue deal collapses as Lindsay Fox opts to go alone

- Banks call for crisis talks as cash transport firm teeters

- Bullock says banks should bear more costs of moving banknotes

- Coles to hoard cash amid fears of Armaguard collapse

- Armaguard boss laments cash rebound that never came

- The billionaire versus the banks: The fight over the death of cash

- Armaguard rejects $26 million lifeline to avoid insolvency as Coles ends pause on cash deliveries

- Cash payments continue to decline as Aussies move to electronic methods, RBA says

- Cash Use and Attitudes in Australia – RBA

- Consumer Payment Behaviour in Australia

- Banks in secret study to dump use of cash; A one-way flight of fancy brag to the Brits